Is Strategy's STRC preferred stock a Ponzi scheme? I break down the bitcoin collateral, capital structure, and why Peter Schiff's argument doesn't hold up analytically.

Peter Schiff recently called Strategy’s STRC preferred equity offering a Ponzi scheme. I’ve looked carefully at the mechanics and the argument doesn’t hold up. Here’s my analysis.

What Peter Schiff Actually Said

On a recent podcast episode, Peter Schiff made a bold claim. He argued that Strategy’s preferred equity products — specifically the STRC “Stretch” offering with its ~11% yield — are functionally a Ponzi scheme.

His core argument: Strategy doesn’t earn operating income to pay dividends, so it must raise new capital from fresh investors to pay existing ones. In his framing, that’s the textbook definition of a Ponzi.

It’s a catchy line. But it conflates two very different things: a fraudulent scheme and a legitimate capital structure.

First, Let’s Understand What STRC Actually Is

Before challenging Schiff’s framing, it helps to understand what STRC is at a structural level.

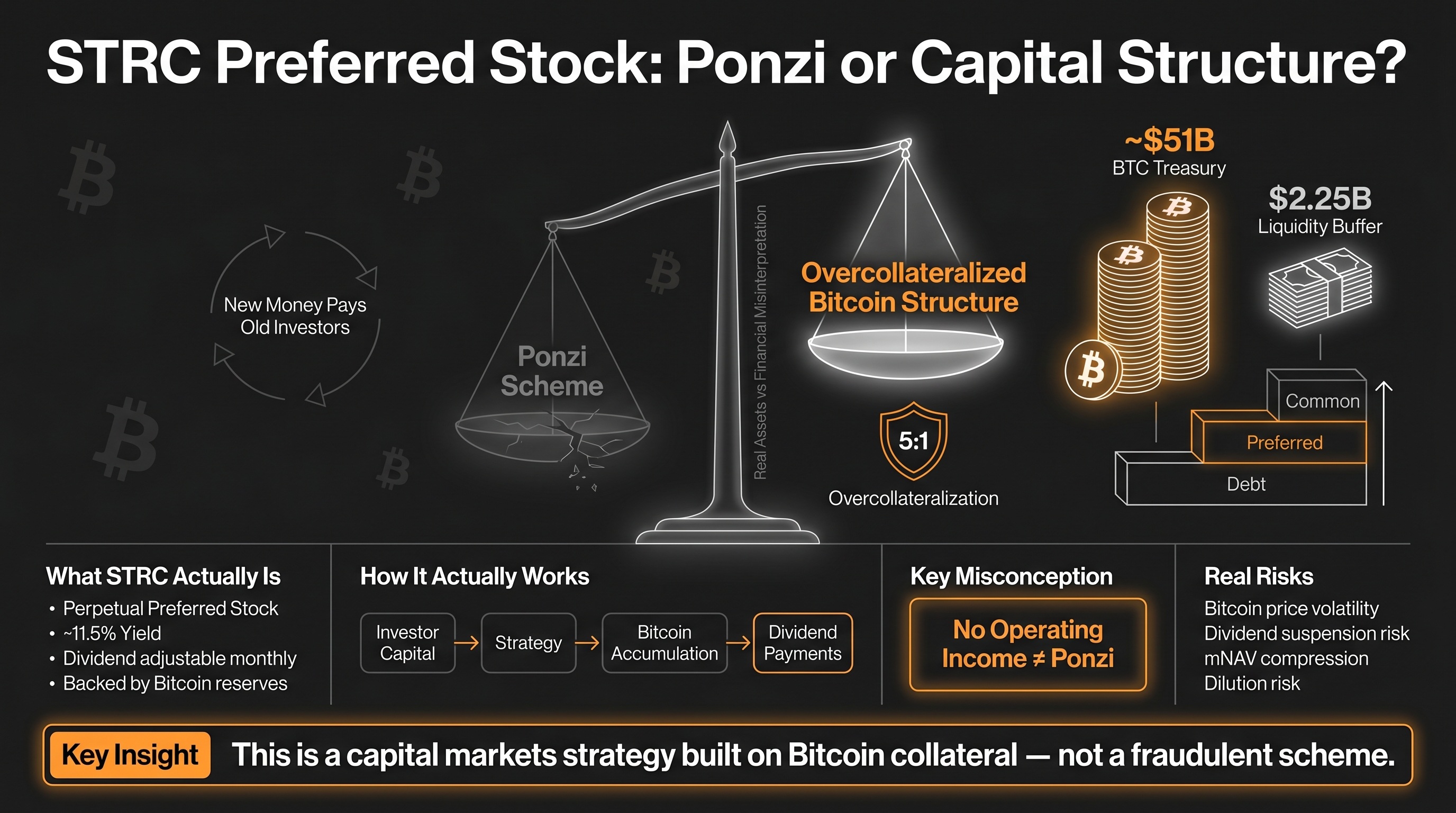

STRC — officially called “Stretch” — is Strategy’s perpetual preferred stock, currently paying an 11.50% annual dividend, distributed monthly in cash. (Source: Strategy.com)

Unlike its fixed-rate siblings, STRC’s dividend rate is variable, adjusting monthly to keep the share price trading near a target of $100 par value. (Source: The Block)

Strategy has the right, in its sole and absolute discretion, to adjust the monthly dividend rate. Dividends are payable when, as and if declared by the board, out of funds legally available. (Source: Strategy.com Press Release)

That last part matters enormously — and I’ll come back to it.

The “Ponzi” Argument, Dismantled

Schiff’s Ponzi framing rests on one assumption: that Strategy has no real way to fund dividends other than selling new shares to new investors. Let me show you why that framing is analytically incomplete.

The Collateral Is Real and Massive

The most important fact Schiff glosses over is the underlying asset backing STRC.

Each share of STRC is overcollateralized with bitcoin at roughly a 5-to-1 ratio — meaning that for every dollar of STRC issued, Strategy holds approximately five dollars’ worth of BTC. (Source: CoinDesk)

Strategy holds 762,099 BTC at an average cost near $75,694 per coin, a treasury valued at roughly $51 billion. That single Bitcoin stack backs both its common stock and its perpetual preferred shares. (Source: CryptoNews.net)

A Ponzi scheme has no real assets. It’s a fiction. Strategy’s collateral is publicly auditable, on-chain, and valued in the tens of billions of dollars. That’s not a fiction — that’s a balance sheet.

Source: X Post - April 26, 2026

The Cash Reserve Is Also Real

Strategy maintains $2.25 billion in cash reserves to service dividend payments, and its BTC treasury dwarfs STRC’s notional market cap many times over. (Source: CryptoNews.net)

Think of it this way. If I own a $50 million apartment building and I borrow $2 million from you at 10% interest, you don’t call that a Ponzi scheme — even if my building doesn’t generate operating income yet. The collateral backs the obligation. The math works.

The Overcollateralization Buffer Is Enormous

The $8 billion in convertible debt and preferred equity obligations are 15x overcollateralized by Bitcoin reserves. Even if Bitcoin’s price were to decline by 50%, the company’s obligations remain comfortably covered. (Source: AInvest)

That’s a dramatically different risk profile than Schiff implies. A true Ponzi collapses the moment new investment slows. Strategy’s preferred obligations could theoretically be serviced from its BTC holdings alone — no new investor required.

The Structural Difference Between STRC and a Ponzi

Let me explain this with a simple analogy. Imagine a family that inherits a large gold mine worth $50 million. They issue $5 million in bonds to investors, paying 10% interest annually. They don’t have a salary — but they have the gold mine. They can sell pieces of it, lease mining rights, or raise capital at a premium to their reserves.

Is that a Ponzi? Of course not. The asset exists. The overcollateralization provides the buffer. The obligation is transparent and disclosed. STRC operates on a similar logic — but with Bitcoin as the reserve asset.

The Capital Markets Strategy Is the Point

What Schiff mischaracterizes as fraud is actually a deliberate capital allocation strategy. Strategy has built a capital markets machine around a single thesis: Bitcoin will appreciate over time.

By issuing convertible preferred equity across STRF, STRK, STRD, and STRC, Strategy raised $18.3 billion in 2025 — achieving 81% of its full-year 2024 total in just seven months. (Source: AInvest)

This is what sophisticated Bitcoin treasury companies do. They use equity and debt markets to accumulate more BTC, with the expectation that Bitcoin’s long-term appreciation more than offsets the cost of capital.

The key question — as I always frame it — is: does this capital raise increase BTC per share? If the answer is yes, it’s accretive to shareholders. That’s not fraud. That’s capital efficiency.

Why the “No Operating Income” Argument Misses the Point

Schiff’s critique anchors on the idea that Strategy doesn’t earn traditional operating income to fund dividends. That’s true. But it’s also largely irrelevant. Let’s think about this from first principles:

• A REIT often pays dividends funded by property sales or capital raises, not solely operating income. Nobody calls REITs Ponzi schemes.

• A royalty company pays holders from asset monetization, not a salary. Nobody questions the legitimacy.

• A closed-end fund may distribute capital gains rather than income. That’s legal and fully disclosed.

Strategy’s model is simply a Bitcoin-native version of these structures. The dividend is funded by a combination of:

• Capital raise proceeds (from preferred stock ATM programs)

• Bitcoin appreciation (which increases the collateral pool)

• Cash reserves explicitly held for this purpose

None of these mechanisms are hidden. All of it is disclosed in SEC filings. That’s the opposite of a Ponzi.

The Cumulative Dividend Feature Is a Feature, Not a Red Flag

One nuance worth highlighting: STRC’s dividends are cumulative and compound if unpaid. This is actually investor-protective — not a warning sign.

If Strategy misses a payment, they don’t escape the obligation — it accumulates. STRC sits senior to common equity and most other preferred series, but junior to debt and the STRF preferred series. The capital stack is clearly defined and legally enforceable. (Source: CoinDesk)

Schiff is right that the board can choose to stop paying dividends. But that’s not deception — it’s standard preferred equity disclosure. The prospectus makes it explicit. Investors who buy STRC know this going in.

What Makes This Legitimately Risky (And What Doesn’t)

To be clear: I’m not arguing STRC is risk-free. It isn’t. The real risks worth noting:

• Bitcoin price risk: If BTC falls dramatically and stays low, the collateral cushion shrinks.

• mNAV compression: If the premium to NAV collapses — see understanding mNAV — the capital markets flywheel becomes less efficient.

• Dilution risk: Continued share issuance to fund BTC purchases may dilute common shareholders over time.

• Dividend suspension: The board can legally reduce or suspend the dividend.

These are legitimate risks that any sophisticated investor should model carefully. But risks are not fraud. And a business model being difficult to understand is not evidence of a Ponzi. Schiff conflates complexity with deception. Those are very different things.

The Institutional Signal Worth Noting

Here’s something Schiff dismisses too quickly: institutions are buying STRC.

He acknowledged this himself on the podcast — noting that some institutional buyers know it might be risky but are chasing yield. But in my analysis, institutional participation in a clearly disclosed, SEC-registered, Nasdaq-listed instrument is a strong signal that the structure passes basic legal and fiduciary scrutiny.

These are compliance teams, lawyers, and risk desks reviewing the prospectus. They’re not naive. And they’re still buying.

Final Thoughts

Peter Schiff is a smart man, and his broader concerns about leverage in the Bitcoin ecosystem deserve a fair hearing. But the Ponzi accusation directed at STRC doesn’t survive analytical scrutiny.

A Ponzi scheme is built on fraud, deception, and non-existent assets. STRC is built on:

• A publicly auditable Bitcoin treasury worth ~$51 billion

• Disclosed, SEC-filed terms with full transparency

• A 5-to-1 overcollateralization ratio on every dollar of STRC issued

• $2.25 billion in dedicated cash reserves

• A legally enforceable, clearly ranked capital stack

That’s not a Ponzi. That’s an unconventional capital structure built around a high-conviction asset — with real risks, yes, but also real collateral.

The right question for investors isn’t “is this a scam?” — it’s “does the 11.5% yield compensate me adequately for the specific risks of this instrument?” That’s a legitimate analytical debate. But it’s a very different conversation than the one Schiff is having.

As I always say: understand the structure, know the risks, and never confuse complexity with fraud.

Check the latest prices of Metaplanet quoted on different exchanges at the link below

Disclaimer:

This article reflects my personal research and opinions and is for informational purposes only. It is not financial advice. I may be wrong, and markets are inherently risky. Always do your own due diligence and consult a licensed financial advisor before making any investment decisions.

Sources

1. Strategy.com — STRC Product Page: https://www.strategy.com/strc/learn

2. Strategy.com — STRC Pricing Press Release: https://www.strategy.com/press/strategy-announces-pricing-of-strc-perpetual-preferred-stock_07-25-2025

3. CoinDesk — Strategy Raises STRC Dividend to 10%: https://www.coindesk.com/markets/2025/09/03/strategy-raises-dividend-on-strc-offering-to-attract-yield-seeking-investors

4. CoinDesk — Why Saylor Calls STRC His iPhone Moment: https://www.coindesk.com/business/2025/08/02/why-michael-saylor-calls-strategy-s-strc-preferred-stock-his-firm-s-iphone-moment

5. The Block — MSTR to STRC Strategy Products Explained: https://www.theblock.co/learn/394455/what-are-mstr-strk-and-strc-strategys-stock-and-preferred-shares-explained

6. CryptoNews.net — MSTR vs. STRC: Which Bitcoin Strategy Fits Your Portfolio?: https://cryptonews.net/news/bitcoin/32650293/

7. AInvest — MicroStrategy Bitcoin Treasury & Capital Markets Q2 2025: https://www.ainvest.com/news/microstrategy-bitcoin-treasury-strategy-capital-markets-execution-q2-2025-2508/

8. Seeking Alpha — STRC: A Variable Rate Preferred Stock IPO: https://seekingalpha.com/article/4809708-strc-a-variable-rate-preferred-stock-ipo-from-microstrategy

9. SEC Filing — Strategy Form 8-K (STRC Dividend Updates): https://www.sec.gov/Archives/edgar/data/0001050446/000119312525225038/d939712d8k.htm