Bitcoin treasury companies hold assets in Bitcoin but liabilities in fiat. I explain how this structure reduces debt burden over time as Bitcoin appreciates.

When I first started analyzing Bitcoin treasury companies, one concept stood out to me immediately. They hold assets in Bitcoin, but their liabilities are mostly denominated in fiat currency. In my analysis, this creates one of the most powerful asymmetries in the entire model.

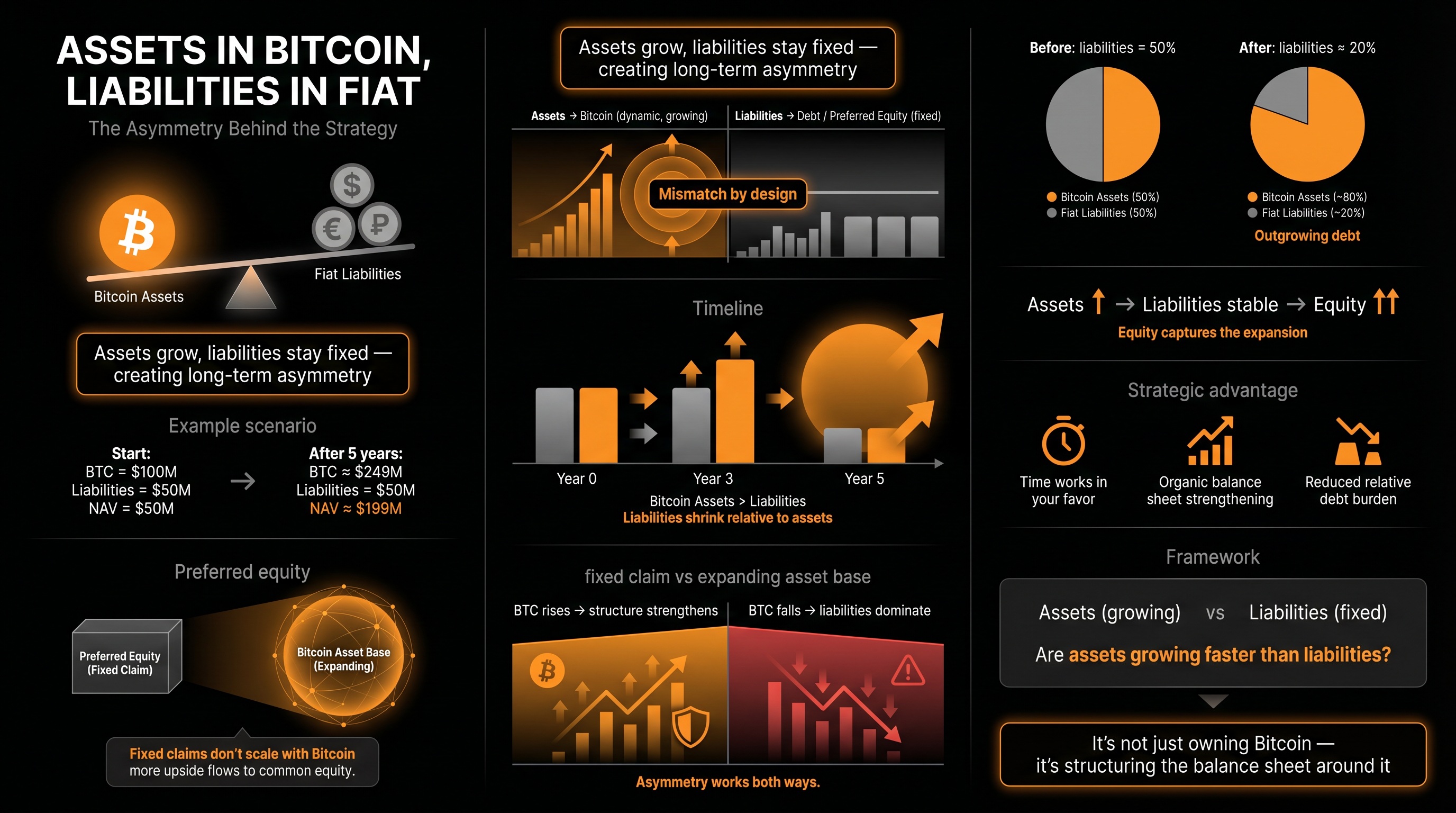

The Core Idea

At a high level, the structure is simple. Companies acquire Bitcoin as an asset, while their obligations (debt or preferred equity) are typically fixed in fiat terms. This means one side of the balance sheet can grow while the other stays relatively constant.

Over time, this creates a dynamic where Bitcoin appreciation can significantly improve the company’s financial position. The asset side expands, but liabilities do not increase at the same rate. This is where the long-term advantage comes from.

Understanding the Balance Sheet Dynamic

To simplify, I break the balance sheet into two parts. On one side, you have Bitcoin holdings, and on the other, liabilities like debt or preferred shares. This framing helps me focus on how each side behaves over time.

The key difference is that Bitcoin is volatile but has historically appreciated over long periods, while liabilities are usually fixed in nominal terms. This creates a mismatch that can work in the company’s favor. In my view, this mismatch is intentional.

It creates a scenario where time becomes an ally rather than a risk. As long as Bitcoin trends upward over time, the balance sheet gradually strengthens. This is one of the core insights behind the strategy.

What Happens When Bitcoin Appreciates

This is where the model becomes powerful. As Bitcoin increases in price, the total value of assets rises, but liabilities remain largely unchanged. The gap between the two begins to widen.

This means the net asset value (NAV) expands over time. More importantly, the relative weight of liabilities decreases. In simple terms, the company becomes less burdened by its obligations.

Even without additional capital raises, the balance sheet improves. Equity holders benefit as the asset base grows faster than liabilities. In my analysis, this is where the asymmetry really shows.

A Simple Example (20% CAGR Scenario)

Let’s walk through a simplified example to make this more concrete. Assume a company starts with $100 million in Bitcoin and $50 million in fiat liabilities. This gives an initial NAV of $50 million.

Now assume Bitcoin grows at a 20% compound annual growth rate over five years. After five years, Bitcoin assets would grow to approximately $249 million, while liabilities remain at $50 million. The change is significant.

What stands out is how the proportions shift over time:

NAV increases from $50M to ~$199M

Liabilities drop from 50% of assets to ~20%

Even though liabilities did not decrease in absolute terms, they shrank significantly relative to assets. This is the key effect I focus on. It’s not about reducing debt, it’s about outgrowing it.

How Preferred Equity Fits Into This

Preferred shares behave similarly to debt in this structure. They typically have a fixed claim on the company, such as dividends or liquidation preference. However, they do not scale with Bitcoin price.

As Bitcoin appreciates, the relative claim of preferred shareholders declines. Common equity begins to capture a larger share of the upside. This shifts value toward common shareholders over time.

In my view, this is why preferred equity can be an effective funding tool. It allows companies to raise capital without immediate dilution of common equity. At the same time, its relative weight decreases as assets grow.

Why This Structure Is Strategic

This structure is not accidental. Bitcoin treasury companies are deliberately aligning appreciating assets against fixed liabilities. This creates a form of financial asymmetry.

If Bitcoin rises, the company benefits disproportionately. If Bitcoin stagnates, liabilities remain manageable in nominal terms. This balance allows companies to operate with a long-term perspective.

From what I’ve observed, this is one of the core strategic advantages. It enables compounding without constant capital raises. Over time, the balance sheet strengthens organically.

The Long-Term Effect on Equity

Over time, this structure shifts value toward equity holders. As assets grow and liabilities remain fixed, equity absorbs most of the upside. This is where amplification begins to show.

In strong Bitcoin markets, this effect becomes more pronounced. Equity value can expand rapidly as NAV increases. Liabilities become less relevant in proportion.

In my analysis, this helps explain why some Bitcoin treasury stocks outperform Bitcoin itself. They are not just exposed to Bitcoin, they are structurally leveraged to its growth. The balance sheet does part of the work.

What Could Go Wrong

This model depends on one key assumption. Bitcoin must appreciate over time for the structure to work as intended. If that assumption fails, the dynamics change.

If Bitcoin declines significantly, asset values shrink while liabilities remain fixed. This increases balance sheet pressure. The same asymmetry that works in your favor can work against you.

In this scenario, equity absorbs the downside more aggressively. This is why risk management is critical. The structure amplifies outcomes in both directions.

My Framework for Thinking About It

I like to simplify this into a basic relationship. Assets are variable and potentially growing, while liabilities are fixed and predictable. The interaction between the two determines outcomes.

The key question I ask is straightforward. Is the growth of assets outpacing the burden of liabilities? If yes, the structure is working.

If not, risks begin to accumulate. This framework helps me quickly evaluate whether a company’s strategy is sustainable. It keeps the analysis grounded.

Why This Matters for Bitcoin Treasury Companies

Companies like Strategy and Metaplanet are built around this idea. They intentionally create exposure to an appreciating asset while keeping liabilities relatively stable. This alignment is central to their strategy.

In my view, this is what makes the model unique. It’s not just about owning Bitcoin. It’s about how the balance sheet is structured around it.

This is where traditional corporate finance meets a Bitcoin-denominated mindset. The structure itself becomes part of the investment thesis. And that’s what makes it interesting to analyze.

My Key Insight

The more I analyze this, the more I come back to one idea. This is a time-based advantage. The longer Bitcoin appreciates, the stronger the balance sheet becomes.

Liabilities don’t need to be repaid immediately, but Bitcoin can continue compounding. This creates a gradual shift in financial strength. Over time, the company becomes more resilient.

This is one of the most elegant aspects of the model. It aligns time, growth, and capital structure in a very efficient way.

Final Thoughts

When I first saw this structure, it seemed simple. But the deeper I went, the more I realized how powerful it can be. It’s a subtle but important design choice.

Bitcoin treasury companies are not just betting on price. They are structuring their balance sheets to benefit from time and asymmetry. And that changes how I evaluate them.

Thank you for reading this insight and I hope you found it helpful.

Check the latest prices of Metaplanet quoted on different exchanges at the link below

Disclaimer:

This article reflects my personal research and opinions and is for informational purposes only. It is not financial advice. I may be wrong, and markets are inherently risky. Always do your own due diligence and consult a licensed financial advisor before making any investment decisions.